How Realistic Are Goldman & JPMorgan’s $4,000 Gold Targets?

JPMorgan and Goldman Sachs’s $4,000 price targets are not only realistic but could even be achieved sooner than they expect.

Despite gold’s strong price gains over the past fifteen months, Goldman Sachs on Monday reaffirmed its forecast for gold to reach $3,700 per ounce by the end of 2025 and $4,000 by mid-2026. If they’re correct—and I believe this projection is quite realistic—that would represent additional gains of approximately 11% and 20% from the current price of $3,331. This is especially impressive given that gold has historically been a relatively low-volatility, slow-moving asset compared to stocks, cryptocurrencies, and other commodities.

Goldman’s main bullish case for gold centers on continued strong central bank and institutional buying. Between January and May 2025, central banks and institutions purchased an average of 77 tonnes of gold per month — just slightly below Goldman’s earlier projection of 80 tonnes per month by mid-2026 in the London OTC market. In May alone, total purchases reached 31 tonnes (excluding the U.S.), with China standing out as the most prominent buyer, adding 15 tonnes. Additionally, Goldman notes that fund net positions in gold have eased from their April highs, creating more room for sustained buying from ETFs and central banks going forward.

JPMorgan agrees with Goldman and last week predicted that gold will average $3,675 an ounce in the fourth quarter of this year, rising to $4,000 in the third quarter of 2026. Previously, the firm didn’t expect gold to reach $4,000 at all next year. Natasha Kaneva, head of global commodities strategy at JPMorgan, explained that the risk of a recession and global trade tensions make the $4,000 target even more achievable. "We remain deeply convinced of a continued structural bull case for gold and raise our price targets accordingly," Kaneva said.

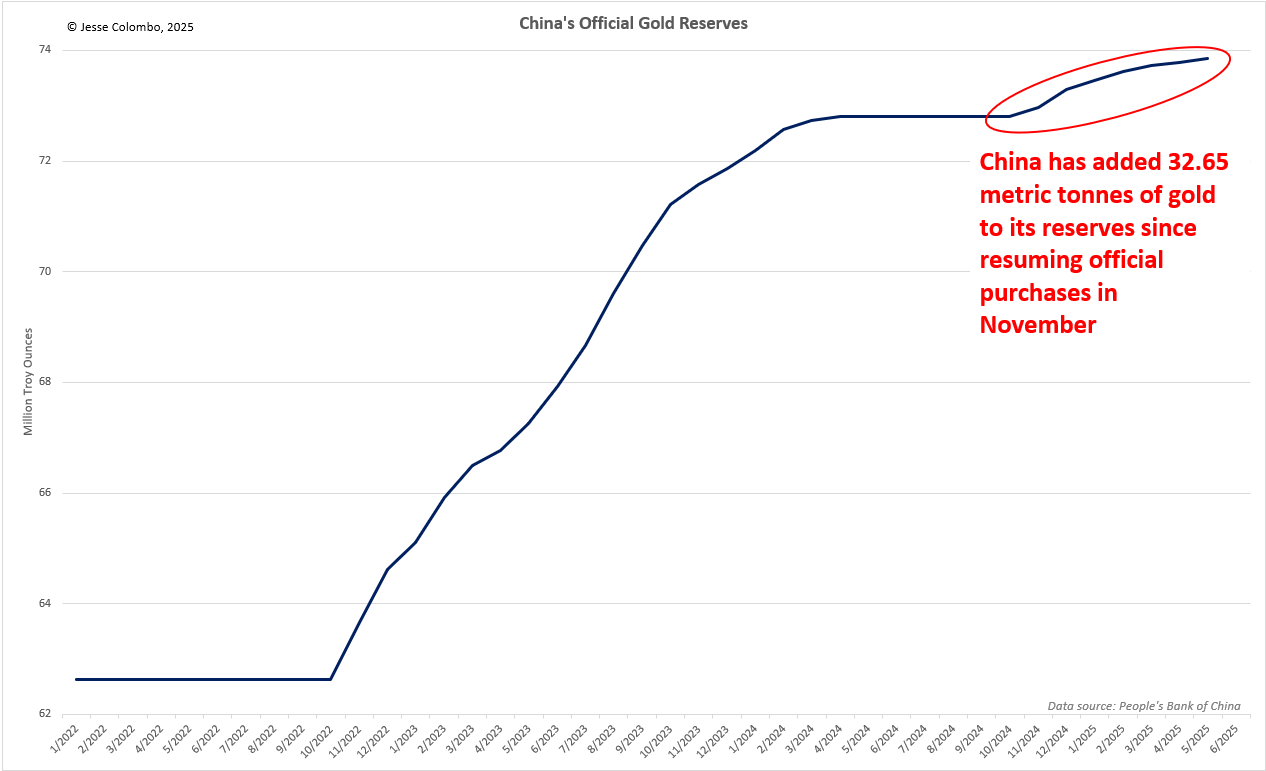

As I have written before, China has been one of the most prominent buyers of gold in recent years, adding 32.65 metric tonnes to its official reserves since November. In reality, China is likely purchasing even more gold than it officially reports, using various discreet channels. The fact that it has been openly reporting increased purchases is likely intended to signal to its citizens and institutions to continue steadily accumulating gold — a sharp contrast to the West, which remains largely indifferent to gold despite its strong gains since early 2024.

Since the pandemic and the ensuing surge in global debt, money supply, and inflation, central banks around the world have significantly ramped up their gold purchases, averaging just over 1,000 tonnes per year in 2022, 2023, and 2024. This marks a dramatic increase — roughly double the annual average of about 500 tonnes in the preceding decade. This trend is expected to continue, supporting higher gold prices as central banks increasingly diversify their reserves into hard assets to safeguard against inflation and the growing economic risks posed by massive global debt levels.